Payroll Paperwork

In order to begin receiving paychecks you must complete all payroll paperwork.

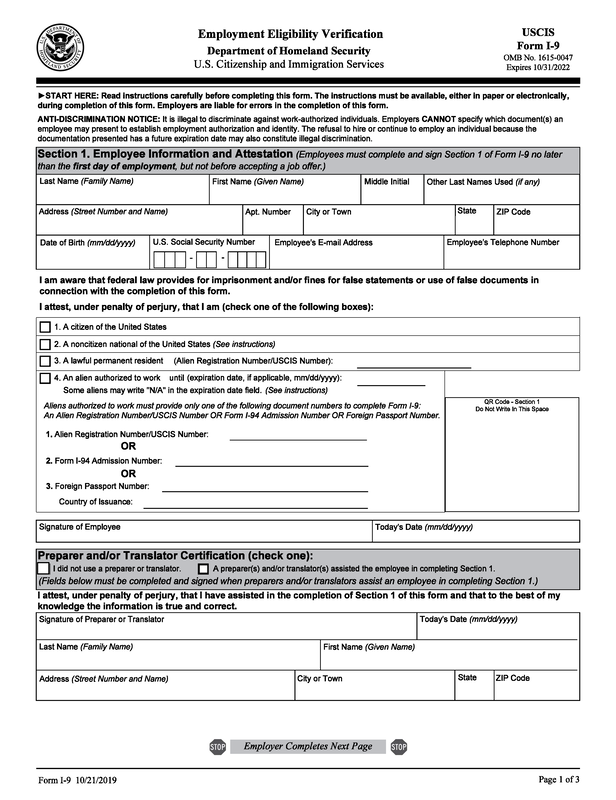

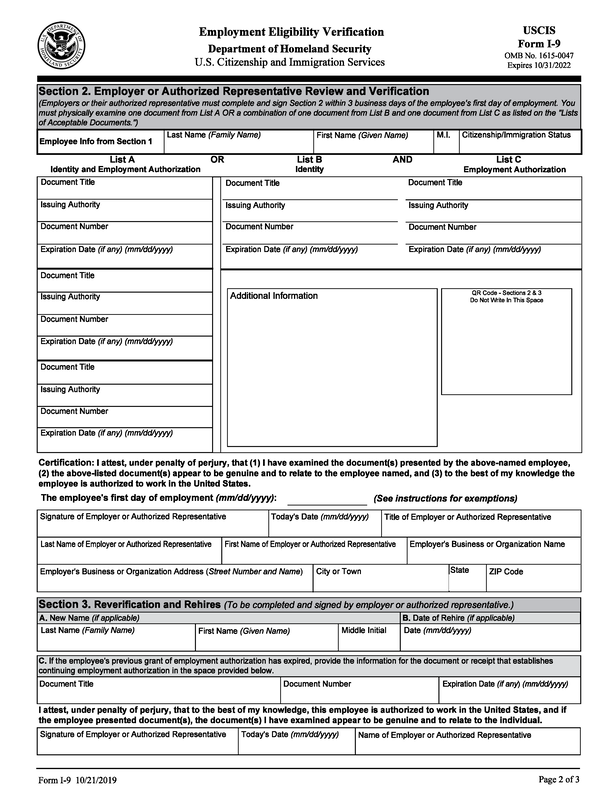

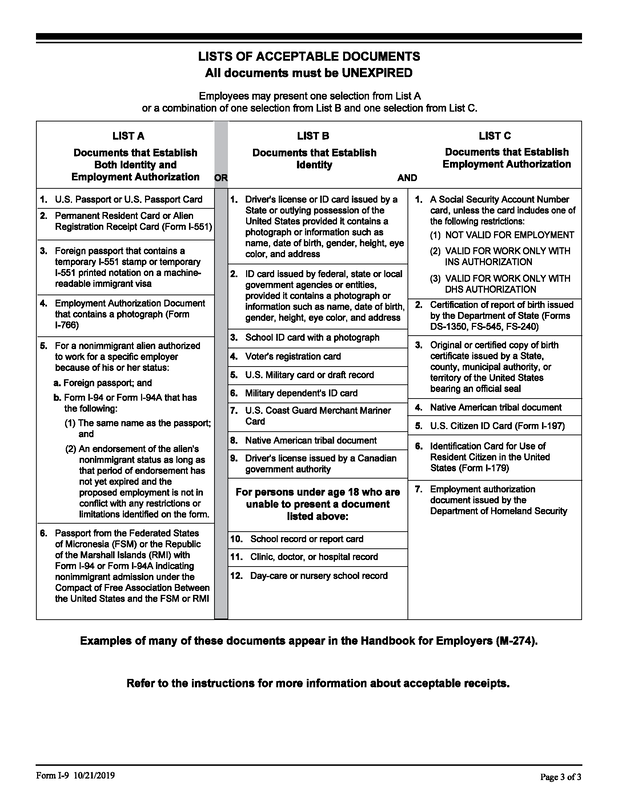

I-9

We will need to keep on file the documents you are using from page 3.

|

|

|

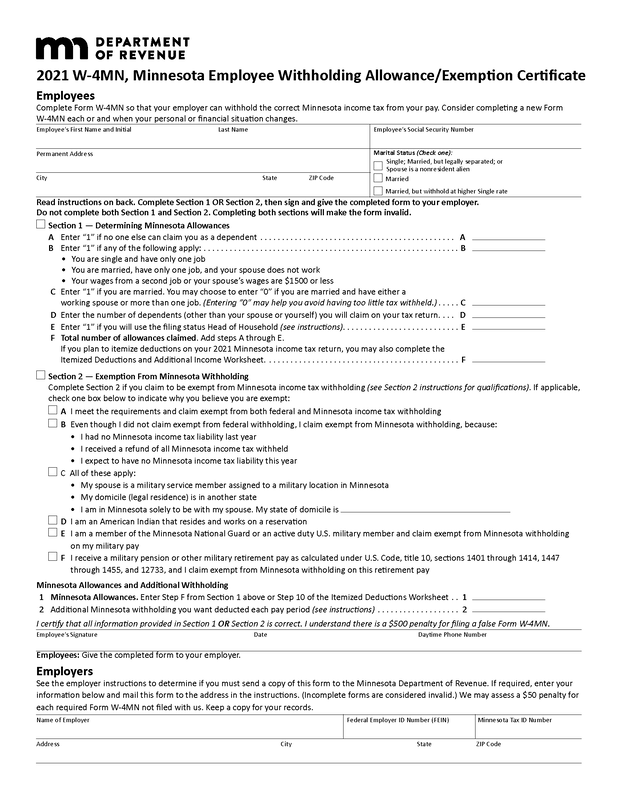

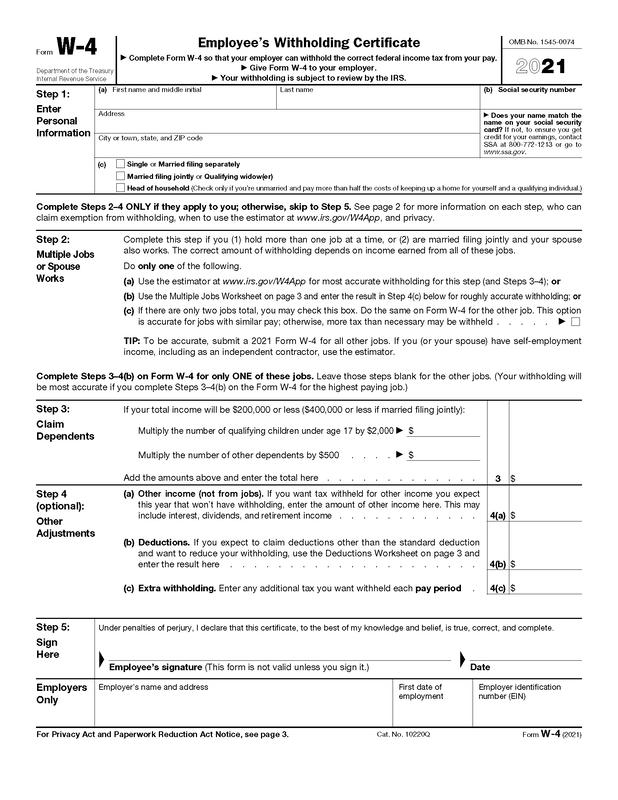

W-4

Both Minnesota and a Federal Form are required

|

|

|

|

|

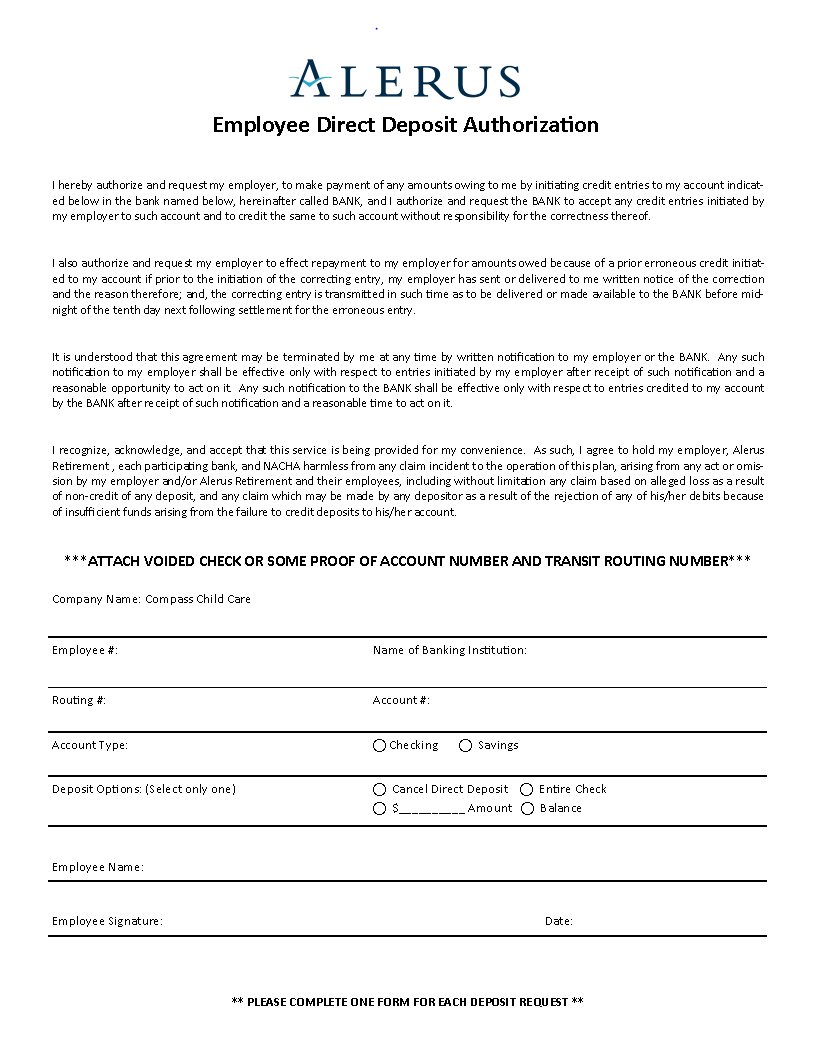

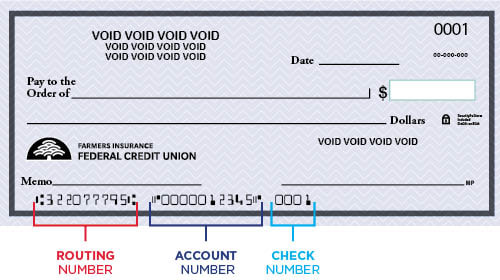

Direct Deposit

|

We pay with Direct Deposit. Payday is every other Friday. If you do not complete the Direct Deposit form your check will be mailed to you. Checks are mailed from our Payroll company on the Friday of payroll. You may not see your check in your mailbox for 3-5 business days.

If you decide to split deposit your check please fill out 2 forms. Examples of this would be: I would like $100 into Savings (one form) and Balance of my check into my Checking Account (2nd form). Another common use is for checking and retirement account. Most common is 1 form- entire check direct deposited into Checking Account. |

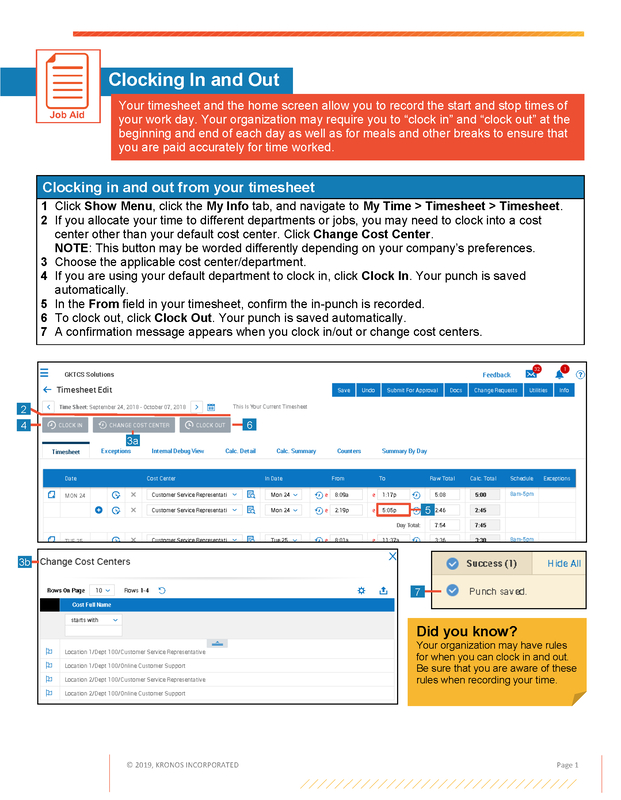

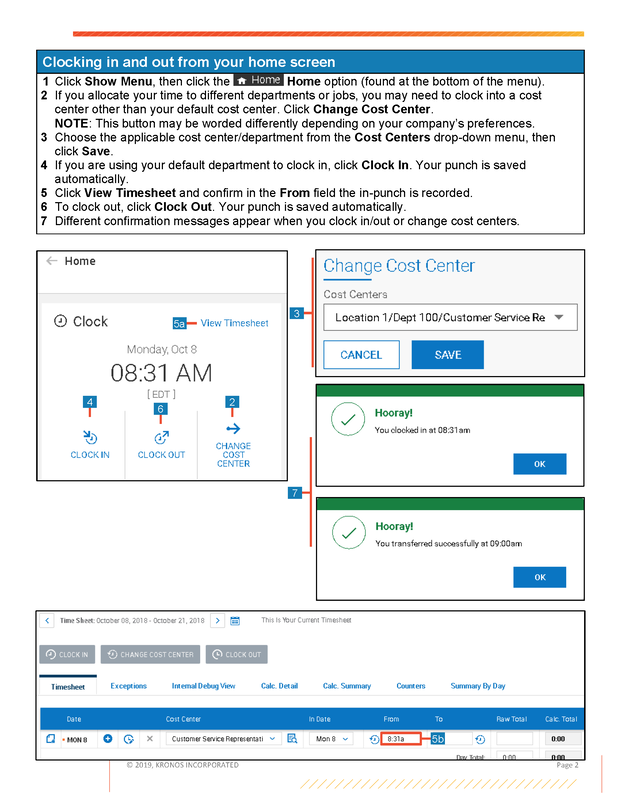

Clock In and Out

You are responsible for clocking in at the beginning of your shift and after break, and clocking out at the end of your shift and at the beginning of your break. If you miss a punch please see management immediately. Each school has a computer designated for clocking in and out. You will get your code via email. There is a short time window when you get that email to set up your account. If you wait too long you may get locked out. Please see site management if that happens!

|

|

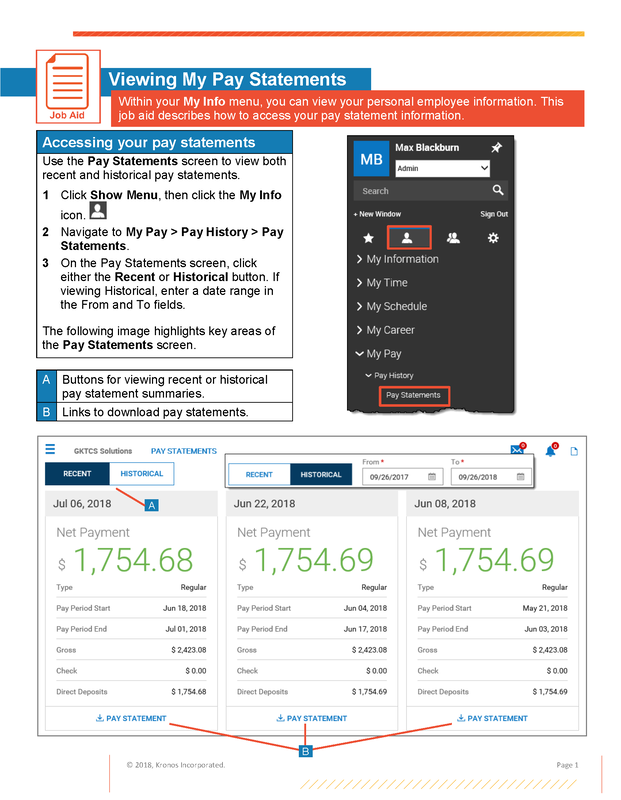

View your Paystubs

You are able to review your statements and download paystubs as needed. If you need help logging in, please see site management!

|

|

*Time off is decided 1. First come first serve and 2. Seniority. When making Dr. appointments please keep in mind: If you are an opener - It is easier for us to let you leave earlier. If you are a closer- It is easier for us to have you come in later.

Benefits

After you have been with us 90 days, if you are now eligible for some benefits.

Health Insurance

If you work 40 hours a week and have been with us for 90 days you qualify for Health Insurance. If you do not want Health Insurance through Compass you will need to sign off on a form that you are declining coverage. See below for the options and additional information.

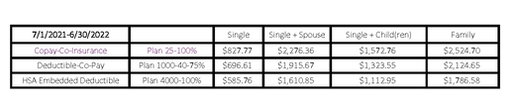

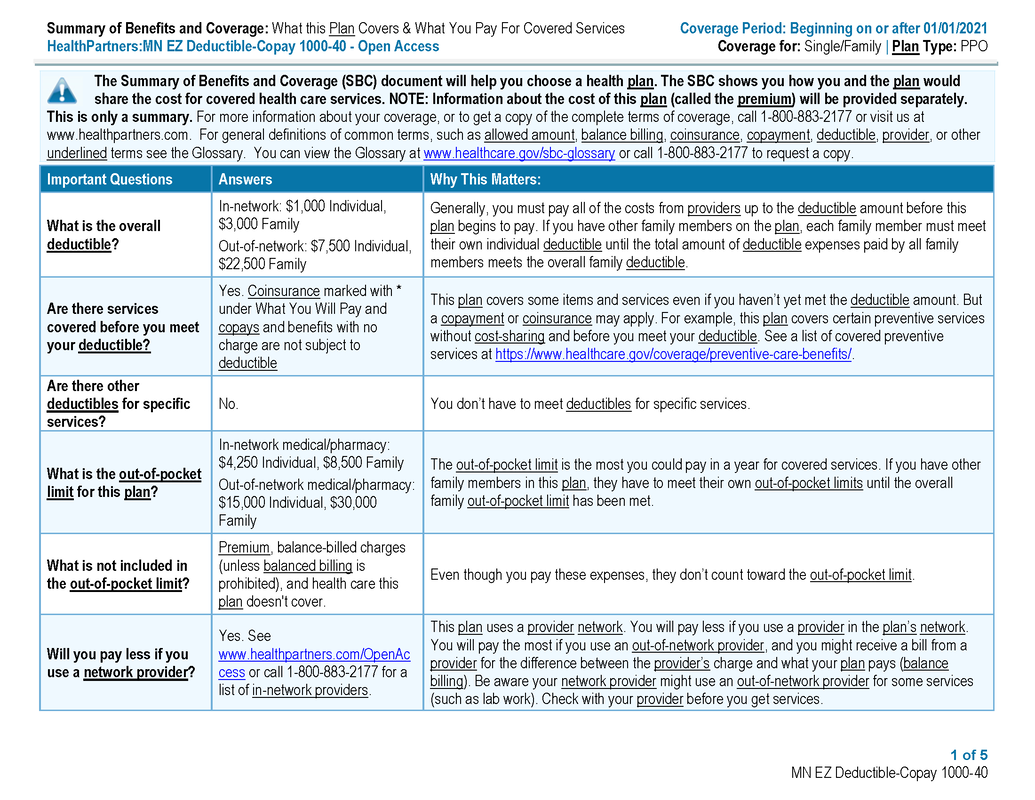

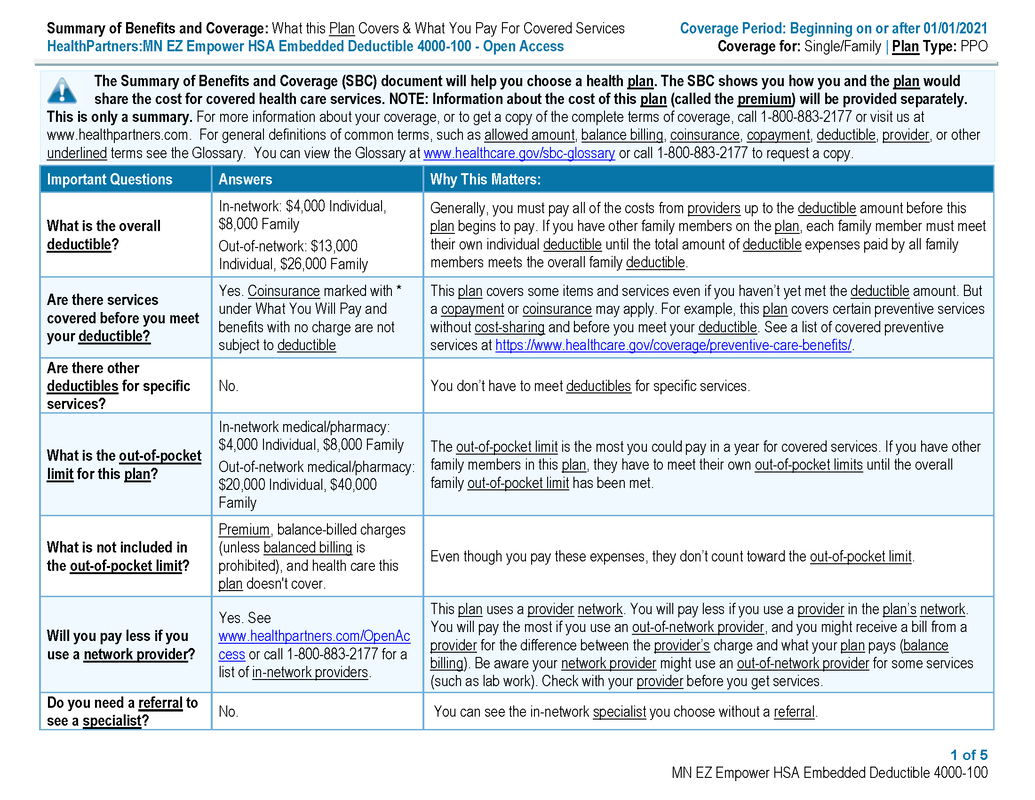

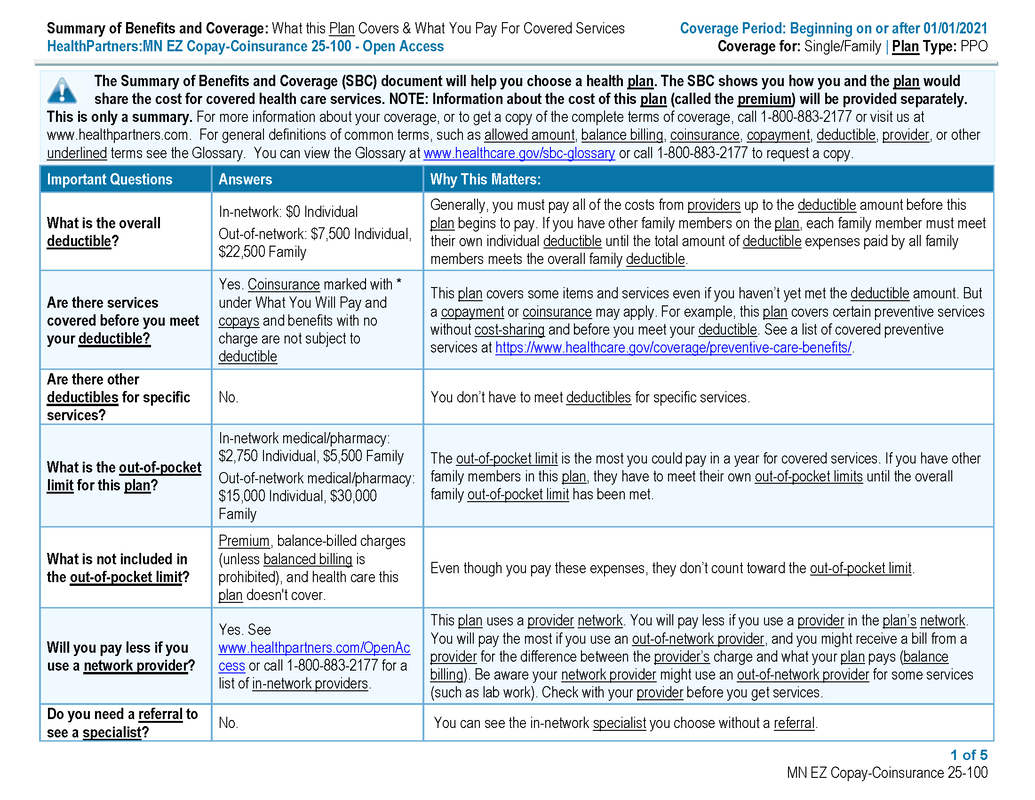

What plan is right for you:

|

A Copay plan has a flat dollar amount that needs to be paid to a health care provider for services rendered. Co-Pays can vary for different services within the same plan, like drugs and visits to specialists. •A co-pay plan sets fixed dollar amounts (called “co-pays”) that you’re required to pay when you go in for medical services. As an example, your plan could have a $20 co-pay for primary care doctors, $40 for specialists, and $15 for generic drugs. When you go to the doctor or refill a prescription, this is the amount you’ll pay, subject to any deductible or co-insurance. You will pay a higher monthly premium to get the coverage benefit of co-pays up front. •Co-pay plans will usually have a co-insurance (the cost sharing with the health insurance company) on higher ticket services, like hospital stays, maternity care, x-rays, etc. •Co-pay plans will still have a deductible and out-of-pocket maximum. Co-pays usually do not count towards the deductible, but they do count towards your annual out-of-pocket maximum. If you reach your out-of-pocket maximum, the insurance company pays 100%, eliminating the need to pay your co-pays. Who do co-pay plans make sense for? •Co-pay plans may make sense for people who don’t make many trips to the doctor’s office, but want the security of first dollar coverage. •These plans also make sense for people who don’t have the budget to pay the full price of a medical bill or prescription out-of-pocket or for people who are willing to pay more each month for the peace of mind in knowing about how much they’ll pay when they visit the doctor. Perks: •Peace of mind knowing how much you’ll pay when you visit the doctor. The rules for health insurance copayments vary, but common services covered are:

Forms you will need

Compass pays 50% of the individual HSA plan. Roughly $292.88 based on these rates. You can apply that amount to any of the 3 plans.

|

HSA Plan A High Deductible Savings Plan – with a health savings account A health savings account is a tax-deferred, tax-advantaged, medical savings account designed to pay for medical expenses with tax-free dollars for individuals who are enrolled in a high-deductible health plan. The funds contributed to an account are not subject to federal income tax at the time of deposit. HSA funds roll over and accumulate year to year if they are not spent (it is NOT a use it or lose it). HSAs are owned by the individual. Earnings on your HSA are tax-deferred – and HSA assets used for qualified medical expenses are never taxed. HSAs allow people to pay for current healthcare expenses and save for future expenses on a tax-favored basis. (premium payments is NOT considered a medical expense) The 2021 annual HSA contribution limit will increase to $3,6000 for single and $7,200 for family 55 or older, $1000 catch up You do not have to contribute to your HSA, but if you choose to do so, you must have some money in the account PRIOR to your first medical expense. You can add to your account all at once, or over time – all contributions for that calendar year must be submitted prior to filing your taxes. Who do HDHPs make sense for? •These plans tend to work well for people who know they’ll meet their deductible early in the year and who can afford to pay the deductible — sometimes in one lump sum — over the course of a year. •HDHPs may also make sense for people who don’t go to the doctor often. These plans typically have lower monthly premiums. For people who don’t expect medical expenses, these plans may be better. Perks: •Lower monthly premiums than co-pay plans. •A health savings account (HSA). This is essentially a savings account where you can put money aside to spend on qualified medical expenses, including deductibles. The money you deposit into a health savings account is tax advantaged, meaning that you can deduct contributions that you make to the account on your taxes. Reimbursements for qualified expenses made from the account are also not taxed. •It may seem like paying “full price” until you meet your deductible isn’t saving you anything out of pocket. However, with a HDHP the insurance company negotiates reduced payment rates with medical providers. That means you’re charged the same amount the insurance company would pay rather than the list price for medical care that you would pay if you didn’t have coverage. Qualified Expenses: Examples of qualified medical expenses include (but are not limited to):

|

AFLAC

AFLAC has short term disability and life insurance. You are required to pay 100% of the cost of these plans but they are a value to you. Many people use the short term disability for a paid maternity leave. If you are interested please see Management to be connected with our representative. This is open to any employee working more than 30 hours a week, for more than 90 days. *There is some fine print on the maternity leave- please be sure to ask a lot of questions before you become pregnant, there is a wait period.

Vacation Time, Holidays and Snow Days

Vacation time is earned after 1 year of employment at 2% of the hours you worked that year (roughly 1 week of your average hours). Starting at your 365th day of employment you begin to accrue vacation time at 4% (roughly 2 weeks of your average hours). Vacation time can not be used during your last 2 weeks of employment and is use or lose. i.e. We do not pay out vacation time if you leave the company.

Holiday pay is earned after 90 days of employment with Compass. You will get paid for the holidays we are closed for IF: you are normally scheduled for the day the holiday falls on & you do not call out (and do not have pre-approved time off) the work day before or after the holiday. Full shift must be worked.

8 hours is the maximum hours paid on a holiday.

Snow days will happen in Minnesota. You will get paid between 4-8 hours on those days if you complete in-service hours in Develop. You must turn in your certificates to get paid. You are not required to work on a snow day, you can take the day off. See Management for assistance with Develop and for a list of approved classes.

Bonuses

Each quarter we release a new set of bonuses. Examples are:

Summer 2021: June 7th-August 31st

Finders Keepers

Attendance (unexcused absence = call outs)

Summer 2021: June 7th-August 31st

Finders Keepers

- If you bring in a staff member that gets a job at Compass you both get $100/month as long as you both still work at Compass. If one leaves, both lose the bonus. New to Compass Hires Only. Bonus can last indefinitely, No limit. You can recruit for any location.

- If you refer a family to join our program you will get $250/month for up to 4 months per child (part time children will earn you $125/month for up to 4 months) You must stay employed and the students must still attend for the bonus to be received monthly

Attendance (unexcused absence = call outs)

- 0 absences $50/payroll

Child Care Discount

Staff Child Care Discount

- No Enrollment Fee charged

- 50% off Infant & Toddler age children

- 75% off Preschool & School-age children

Career Advancement

Through the Develop platform we can reimburse you for classes that will help you become Assistant Teacher or Teacher qualified. If you are 18+ and aide qualified but want to move up, please see your director for help with Develop and information on how the Track 2 Variance works.

Compass is always growing, with that growth we are looking for people interested in management. We have a Director in Training program that help's Teacher qualified staff achieve their management dreams. If you would to be on that track please let your site management know!

Compass is always growing, with that growth we are looking for people interested in management. We have a Director in Training program that help's Teacher qualified staff achieve their management dreams. If you would to be on that track please let your site management know!

Coming Soon

- 401K

- Tuition Reimbursement